Rising Costs Impact Workers and Employers

Deductibles are increasing; employees are being asked to pay more; and employers’ health plan costs are still rising faster than the consumer price index (CPI).

Matthew Rae, senior policy analyst for the Health Care Marketplace Project of the Henry J. Kaiser Family Foundation, shared highlights of Kaiser’s Employer Health Benefit Survey 2015 during The Alliance Employer Benefits Roundtable at Monona Terrace on Dec. 1.

Rae focused on the rising costs impact on workers, employers and employer-sponsored health plans, which cover 57 percent of non-elderly Americans.

Contributions Outpace Workers’ Pay

Health care rising costs impact workers and employers. Rae pointed out that over time, workers’ health care costs have steadily increased. From 1999 to 2015, the Kaiser study shows:

- A 203 percent increase in health insurance premiums

- A 221 percent increase in workers’ contribution to premiums

- A 56 percent increase in workers’ earnings

- A 42 percent increase in overall inflation.

“The worker contribution has grown almost five times faster than workers’ earnings over that period,” Rae noted.

How Employer Size Impacts Contributions

Rae said there are “really important differences” in how employers of different sizes tend to approach workers’ contributions to health premium costs.

For example, 45 percent of small firms with three to 199 employees make the same contribution whether an employee enrolls in single coverage or family coverage. Only 34 percent contribute more for family coverage than single coverage.

Large employers, defined as 200 or more employees, are more likely to treat those two types of coverage differently. Just 17 percent contribute the same amount to single and family coverage, while 67 percent contribute more for family coverage than single coverage.

Rae noted that more large employers were self-funded..

Deductibles Continue to Rise, Costing Workers and Employers

A large majority of workers, or 81 percent, are now paying a deductible. That compares to 55 percent in 2006.

The average deductible for all workers – a group that includes people with coverage that has no deductible – is now over $1,000. Pare that group to covered employees who already are enrolled in a plan with a deductible, and the average amount rises to $1,318.

In 2015, 46 percent of all workers are enrolled in a high-deductible health plan (HDHP) with a deductible of $1,000 or more for single coverage. That rate changes significantly based on the employer’s size, with 63 percent of workers at small companies with three to 199 workers enrolled in an HDHP, compared to 39 percent at large companies with 200 or more workers.

While $1,000 may seem like a high deductible, it’s still below the deductibles for many federal exchange plans. The average deductible for plans with a combined medical and prescription drug benefit is $5,328 for a bronze plan; $2,556 for a silver plan; $845 for a gold plan; and $69 for a platinum plan.

Focusing on Self-Funding to Help with Rising Costs

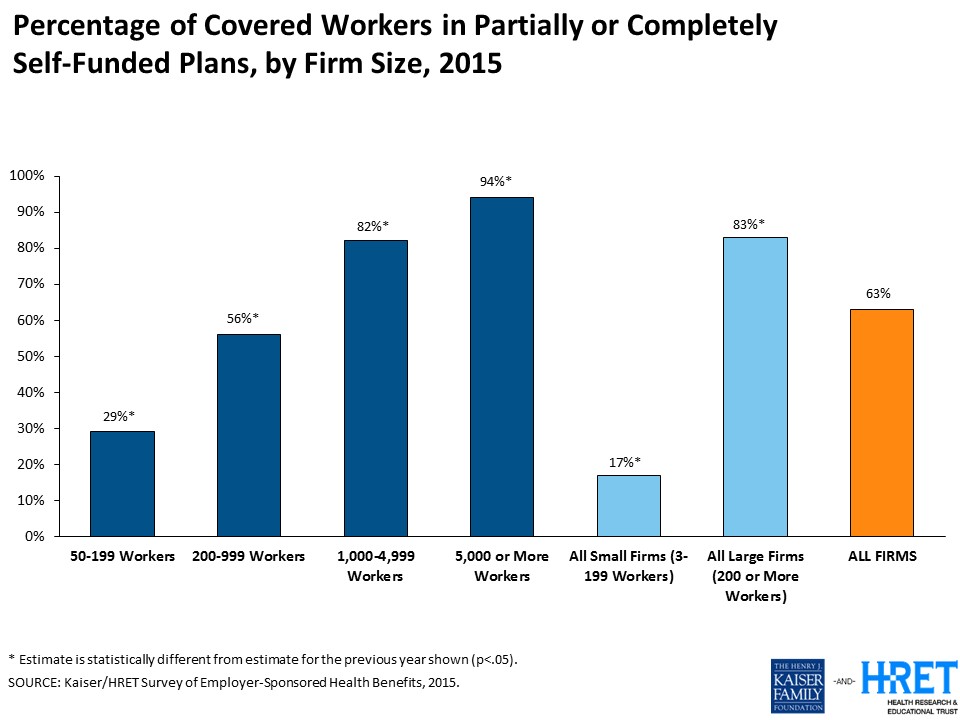

Rae also honed in on the role of self-funding in providing coverage to employees with four charts created for The Alliance event.

At small companies with 50 to 199 employees, only 29 percent of covered workers are in partially or completely self-funded plans, which steadily increases with the company’s size to reach 94 percent of companies with 5,000 or more workers.

Those larger firms are the least likely to purchase stop-loss insurance, possibly because they are better able to bear any losses themselves. Overall, 60 percent of workers were covered by a self-funded plan that purchased stop-loss insurance in 2015.

Anticipating the Excise Tax

Rising health costs increase the likelihood that employers’ health plans will trigger the 40 percent excise tax. This non-deductible tax is 40 percent of the value of employer-sponsored health coverage that exceeds certain benefit thresholds – initially, $10,200 for self-only coverage and $27,500 for family coverage in 2018.

Another Kaiser study shows that among small firms with three to 199 workers, 25 percent will have at least one plan that triggers the tax in 2018; 29 percent in 2023; and 41 percent in 2028. Among large firms with 200 or more workers that rises to 46 percent in 2018; 56 percent in 2023; and 68 percent in 2028.

Large employers are already anticipating the excise tax. More than half of these firms, or 53 percent, have conducted an analysis to see if their plan will trigger the tax. Thirteen percent have made changes to the plan to avoid exceeding limits; 8 percent have switched to a lower-cost plan and 6 percent have taken other measures.

In contrast, 71 percent of small firms have yet to act. Only 17 percent have conducted an analysis, 7 percent have made plan changes and 8 percent have switched to a lower-cost plan.

That is likely to change as the excise tax draws nearer and more health plans are at risk of triggering the tax.

“Obviously, health costs are growing faster than anything else,” Rae said. “So obviously, over time, more and more employers will be subject to the excise tax.”

Excise Tax Could Spur Plan Changes

Among firms who have made plan changes, large firms have taken various steps to avoid the excise tax including increasing cost sharing, a step taken by 64 percent; reducing the scope of covered services, 10 percent; moving to account-based plans such as health savings accounts or health reimbursement accounts, 34 percent; increasing incentives for workers to use less-costly health care providers. 18 percent; and considering offering insurance through a private exchange, 16 percent.

Meanwhile, cost pressures on employers are still in place, which means workers’ share of costs might continue to increase. U.S. health care spending per capita has remained at low rates in recent years, including the 4.4 percent increase in 2015, but Rae noted those rates are expected to rise faster in the years ahead.

[box]

Learn More about Rising Costs Impact Workers and Employers:

- Resources from our past event High-Value Health Care: The Intersection of Quality and Cost

- Read the blog Employees Wary of Out of Pocket Health Care Costs and Look Upstream to Change the Cost and Outcomes of Care

[/box]

Related Posts