How to Evaluate a Provider Network for Your Health Benefit Plan in Three Steps

Every bidder for your health plan’s business claims their network of hospitals, doctors and health services will save you money. But how do you know whether that’s true or just marketing hype?

Evaluating a provider network can have a huge impact on your health benefit costs. Most organizations that consider a network change are trying to solve one of these two problems:

- You are now fully-insured and want to learn whether moving to a self-funded health plan will save money.

- You are already self-funded and want to learn whether switching networks will save you money.

In either scenario, taking these three steps can help you determine whether a network change will genuinely lower your costs.

Step 1: Figure out how the networks differ so you can evaluate what matters.

There can be big differences between networks that impact savings. These differences may include:

- Geographic coverage. This will include not only the territory covered, but the type of providers available in specific communities. The network might have doctors but not hospitals, for example.

- In-network providers. The geographic area covered by the network could be large, for example, but might only contain providers from a single health system.

- Contracting philosophy. For example, a network may emphasize inflation controls, paying for performance or aiming for high-value care. Or, the network may focus solely on discounts.

- Negotiated discounts. A network might have a high discount rate with some rarely-used providers, but offer less savings with providers who deliver the most care for your covered lives.

Comparing and contrasting multiple elements of each network will help you find the best choice based on your health plan goals.

Step 2: Use industry standards to determine whether you are objectively comparing and contrasting each network.

Some networks produce “disruption reports” that emphasize scenarios where they come out on top. But that approach is unlikely to produce cost projections that translate into real-time savings. Your goal should be to compare networks in a way that shows where they differ and what that means to you in health plan dollars.

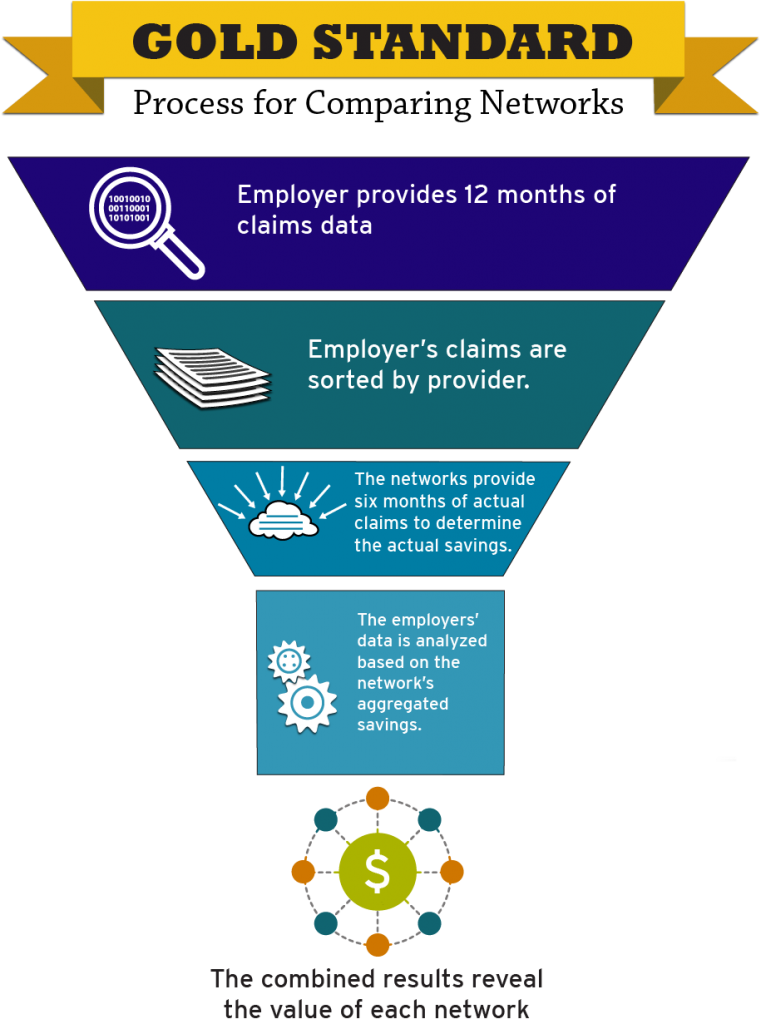

Using the “gold standard” process to evaluate a provider network is likely to produce the most reliable results. Here’s how it works:

- The employer provides 12 months of claims data, based on how covered lives actually used health care services. This data will show how they actually used care, including what types of care were used and which doctors, hospitals, health systems provided that care.

- The employer’s submitted claims are sorted by each in-network provider based on each provider’s tax identification number.

- Each network provides a database of six months of actual claims, which are also sorted by each in-network provider based on each provider’s tax identification number. These claims show the actual savings produced by the discounts included in contracts for health care services.

- The employer’s data is analyzed based on the network’s aggregated savings. This will project what savings can be expected based on covered lives’ actual use of services.

- The combined results reveal the value of each network’s agreements with providers. The results should show both the overall discount achieved by the network and the dollars that the employer can expect to save, based on the submitted claims.

What’s A Provider Disruption Report?

A Provider Disruption Report shows how switching networks will impact your bottom line. Also known as a “claims repricing report,” it should explore:

- How a network change will impact covered employees and family members based on their current use of doctors, hospitals and other health services.

- Which health systems are in-network and out-of-network.

- The savings and discounts that will result from switching networks. Because methods of calculating savings and discounts will differ, it’s important to use the “gold standard” process to obtain an “apples-to-apples” projection.

Step 3: Ask the Right Questions to Evaluate a Provider Network

Networks often submit reports that contain big differences in projected savings and discounts. This is more likely to occur when a network uses a “proprietary” disruption report process that favors its own network.

Asking these questions to help you evaluate a provider network can reveal vital differences between networks and their savings projections.

- How are discounts calculated? Check the process against the gold standard.

- Does the discount evaluation use billed charges or paid charges? The network discount delivered by the network’s provider contract should remain the same either way; however, using billed charges will result in lower projected total savings than using the paid amount.

- Is the impact of your plan design included in the savings projections? Your plan’s excluded services, patient copays and co-insurance will greatly impact your total charges. So your plan design should always be figured into savings estimates. When it is not, network savings are likely to appear artificially high.

- Did the evaluation use the average area discount or a specific discount for a specific provider? Using specific discounts with specific providers is always best. Savings should be calculated based on the doctors, hospitals and health services that your employees and family members are actually using. Some networks will instead use an average that includes their “best” savings or discount rates, even when they are not relevant based on actual usage. Again, the result will be an artificially high savings estimate.

To learn more about self insured health plans, check out our Smarter Self-Funded Health Plans page or email me – I’d love to answer your questions!

Related Posts

Amy Moyer

Amy Moyer was manager of value measurement for The Alliance. In her role, she managed and executed cost and quality measurement and reporting strategies for The Alliance and its members. She's played a critical role in developing The Alliance's QualityPath® initiative. She also participates in state and federal measurement initiatives. Prior to joining The Alliance, Amy served as the quality program administrator at Physicians Plus Insurance Corporation. She took on the role of project manager for the National Committee for Quality Assurance (NCQA) accreditation efforts as well as the development and reporting of key health plan quality metrics. Her resume also includes work at UW Health (University of Wisconsin Hospital and Clinics) where she served as a clinical content facilitator. Amy attended University of Wisconsin-Platteville where she received her Master of Science in project management and Lawrence University where she received her Bachelor of Arts degree in music, neuroscience and biomedical ethics.

See More Posts